Your home stopped being a house. It became their data — and the revenue stream they are fighting over.

On May 20th, a Chicago-area MLS pulled Zillow’s listing feed and 43,000 home listings went dark across the Chicagoland market. A federal judge restored access two days later. The Real Estate of NVA blog, Buyers Locked Out — Two Billionaires Fighting Over Your Listing, covered that event and the local data behind it. The story did not slow down. A Tennessee-based MLS that opened its service nationally on April 30th threatened to cut Zillow’s feed on June 1st, extended that deadline to June 8th, and as of this writing has not yet executed the cut while a new licensing agreement is negotiated. Two MLSs in five weeks. Same orchestrator. Same playbook.

This post focuses on what the headlines keep missing — the structural shift underneath the lawsuits, and what it means for sellers, buyers, and working agents in Northern Virginia.

Three findings drove this analysis:

- The fight is not about private listings. It is about data and revenue. A listing used to be the vehicle that sold the seller’s home. It has been re-engineered into a data asset to monetize attention — by selling leads and selling tours to unprepared browsers.

- The pattern is now visible. Four large regional MLSs in five weeks have partnered with one brokerage — roughly 185,000 agents under MLSs Compass has just brought into the same orbit, including Bright MLS, the regional MLS that serves Northern Virginia.

- The receipts contradict the marketing. Pre-market deals represent under 6% of completed Fairfax County closings in April. Pre-market homes also carry concessions 57% more often than open-market homes, and those concessions average 39% larger. The premium the strategy claims to deliver is partially recaptured at closing in a less visible line item. The advocate is not the leader and the headline does not survive a second look at the data.

WHAT THIS ANALYSIS COVERS:

▸ Why You Should Care — three reasons this story reaches outside the immediate impact zone

▸ Hud’s Take — the disease (fiduciary inversion) vs. the symptoms (lawsuits and rule fights)

▸ Methodology Framing — what this analysis is, what it is not, and how it was cross-validated

▸ The Inversion, Explained — when the listing stopped serving the seller

▸ The Symptoms — MLS rule fights, the end-around, the platform-vs-MLS war

▸ The Land Grab — what 100+ brokerages did when the Chicago feed went dark, and what their motive reveals

▸ The Receipts — local Fairfax County data — who executes the strategy

▸ The Price Story — where the premium lives, where it gets recaptured, and what the data really says

▸ The National Pattern — four MLSs, ~185,000 agents, a coordinated regional campaign

▸ What Actually Wins — the Four P’s of Marketing — the constructive close

▸ The Synthesis — who paid, who is paying next, and the one question left to answer

Why You Should Care?

This story sits in a federal courtroom in Chicago. The local relevance is not obvious until you trace the structure.

▸You may be selling or buying in the next 12 months. The rules under which your home becomes visible online are being reshaped right now by parties whose interests are not aligned with yours. Knowing how the data flows lets you ask the questions that protect your equity.

▸Bright MLS — the regional MLS that serves Virginia, Maryland, DC, Delaware, and parts of three other states — entered the same partnership group on May 13th. Bright’s leadership has so far framed the partnership as cooperation rather than weaponization. Whether posture matches play over the next quarter is a fair question for every Northern Virginia seller to keep watching.

▸The Federal Trade Commission already sued Zillow and Redfin in September 2025 over a separate agreement alleging suppression of competition in rental advertising. The structural concerns named by federal regulators about portal dominance are not hypothetical.

▸You are likely already using the “easy button” — the schedule a tour click on a portal listing. Understanding what that click triggers is the difference between hiring an agent who works for you and being routed to one who paid the platform for your contact information.

HUD’S TAKE:

PRO: I am for pre-marketing as a strategy when it is data-driven and serves the seller’s specific situation. I have represented the buyer on an off-market deal that worked. Let sellers test the market while a home is being prepared — under construction, mid-renovation, cleaning, moving out, repair, condition — at a price that takes it off the market as-is, with no clock ticking. Full marketing. Full touring. Then let it go Active in whatever state the seller calls finished, with the clock starting and the market speaking. We do not need a tracking system for the pre-market preparation window. We need transparency from the moment a home is presented to the open market. The tools are not the problem.

ANTI: I am against using those same tools to conceal data, dodge accountability, and re-route the seller’s home into a brokerage’s lead-generation funnel. The current debate is not really about giving sellers more choice. It is about defining the rules of engagement to favor whichever party wrote them — a tech company (the MLS), an advertiser (Zillow), or a brokerage pulling the strings (Compass). None of those three were hired by the seller. Only the agent was. And every layer of governance that benefits the platform, the portal, or the parent brokerage at the expense of the seller’s exposure is the disease, not the cure.

REASONING: The headlines treat the Zillow-Compass lawsuit, the MLS feed cuts, and the portal partnerships as the story. Those are the symptoms. The disease is older and simpler: the industry started treating the listing as proprietary IP to be monetized rather than as a fiduciary vehicle to sell the seller’s home. Once that inverted, everything downstream — the rule fights, the feed cuts, the velvet-rope private networks — became inevitable. And the contradiction at the center of the current dispute is staring at us in the public record: on the May 5th Compass earnings call, Reffkin told investors that listings on compass.com “are available by request, and they are publicly marketed.” Then his partner MLSs began cutting Zillow’s feed precisely because Zillow treats them as publicly marketed and applies its standard listing-display rules. He cannot have it both ways — privately marketed when convenient, publicly marketed when convenient, and absent days-on-market tracking always. Call it what it is: an extended Coming Soon window with the clock paused. Allow that. Then let the open market speak.

The closing question I keep returning to: Who is actually managing your home listing — and whose revenue depends on what they do with it?

METHODOLOGY FRAMING

This analysis combines national reporting from named, freely-accessible sources (CNN, The Real Deal, HousingWire, Real Estate News, Inman, RISMedia, FTC.gov, Motley Fool earnings transcripts) with original local research pulled from Bright MLS data covering Fairfax County and Reston for April 1st – May 6th, 2026. The brokerage-by-brokerage breakdown of 0–1 days-on-market transactions, the sale-to-assessed comparisons, the concession-rate analysis, and the local rate of pre-market activity are Hud’s primary research and have not been previously published.

The 0–1 days-on-market metric is a behavioral proxy for pre-market execution — under Bright MLS’s rules, a transaction that closes within one day of going Active was substantially completed in the Coming Soon or Office Exclusive window before the home was publicly visible. The proxy is directional, not absolute. The 2026 local findings independently replicate Bright MLS’s own April 2025 regression on more than 100,000 sales.

THE INVERSION EXPLAINED

The listing used to serve the seller. Now, for parts of the industry, it serves the platform and the brokerage.

Then: the listing was the tool. The agent’s job was to get the home in front of every possible buyer, because broad exposure drives competitive offers, and competitive offers drive price. More eyes, better outcome.

Now: for a growing slice of the industry, the listing serves the platform and the brokerage. Keep the listing inside the house first. Show it to the brokerage’s own buyer pool. Double-side the commission when possible. Feed it to a portal so the portal can generate buyer leads — leads the agents then buy back through programs like Premier Agent and Flex. Drive engagement, capture data, monetize attention.

The tell is the revenue source. When money flows from the transaction — selling the home — the seller and the agent are aligned. When money flows from the data and the attention — the leads, the clicks, the tours — the home is no longer the product. The reader is the product. The listing is the bait.

Compass CEO Robert Reffkin told CNN on April 26th, 2026: “The secret to Compass’s success is knowing that the real estate agent is the client.” Not the buyer. Not the seller. The agent. That sentence is not a scandal. It is an honest description of who the model serves.

THE SYMPTOMS — NOT THE STORY, BUT WORTH NAMING

Once the listing became data to monetize, the contortions followed.

The MLS rules that contradict themselves. In most markets, including Bright MLS in Northern Virginia, sellers and agents are forced to choose between three legitimate goals:

- A Coming Soon listing is visible to other agents and may be publicly marketed, but not toured without a clock ticking.

- An Office Exclusive can be marketed and toured without a days on market clock or pricing history, but is invisible to other brokerages and may or may not be syndicated. None of that arrangement protects the seller. It protects listing-fee revenue and brokerage control.

- The End-Around. Here is the move the current legal fight is really about: a brokerage advertises a home privately within its own walls first — working it off-market — then drops the listing into the MLS late, as Coming Soon or Active, once a buyer has already been lined up or to go on the open market. The home appears to sell in one day. It did not. It was sold before the public ever saw it and was recorded for agent / brokerage stats and market comparison purposes only or it is going on the open market (>90% of off market listings end up on the MLS).

The kicker is that the brokerage holds it “off market” for a period of time, then chooses to want to use the feed from the MLS to Zillow, off market, (acknowledging this is the best marketing machine with the most eyes on the market) and later marks the home active because either it sold or it still needs to sell and again wants the feed from the MLS to Zillow.

Brokerage Overreach. What the brokerage does not like is the Days on Zillow or a Price on Zillow. Brokerages are now trying to write the rules for an advertising platform and create complexity in the listing for their perceived monetary benefit. Honestly, I personally do not require the knowledge of Days on Zillow or a Price on Zillow to know this is merely an Auction Price, a place to start, in order to understand fair market value for the condition of the home in a negotiation. The Market Always Speaks and Determines Price.

Zillow’s Overreach. Zillow’s response was to announce a rule: any home marketed to consumers must appear on Zillow within one day, or be banned. But Zillow is an advertising portal. It lives entirely on the feeds it is given, and has no way to manually see a listing that was advertised privately and never fed to it. The rule is therefore largely redundant with what the MLS already governs — except as a weapon aimed at the private end-around. And the only way Zillow can enforce that weapon is the blunt instrument: cut the brokerage’s feed. That club is exactly what set off the events of the last six weeks.

The Retaliation. On May 20th, a Chicago-area MLS cut Zillow’s entire regional feed. The Compass CEO then ran a multi-day social-media campaign against Zillow for “not having all the listings” — while citing screenshots from a city where his brokerage did not have private listings to fight over. All three players — the brokerage, the MLS, and the portal — put their revenue war ahead of the 43,000 sellers (and at least double that number of buyers) whose homes briefly disappeared from the largest search platform in the country. If you think it sounds like a childish school yard fight at recess, you would be right.

Ask the agent how “protecting data” benefitted the consumer and how do they explain the fight. Does the explanation include so that the listing brokerage can receive the phone call when “the easy button” for a tour is clicked and a bonus payment at the sale for advertising and the direct referral of the buyers?

Not all states support Dual Agency (same agent for both sides of the transaction) or Designated Agent (same brokerage represents both sides of the transaction) and double compensation. The agent can refer to someone else and still receive a referral payment instead of Zillow making a referral. Double Seller Brokerage Comp and / or Referral Comp.

Or it may be brokerage payment from Zillow for those listings “sold as leads” to Zillow Premier, Flex agents that brought the buyer, meaning Zillow was paid by the buyer’s agent for the lead that closed and Zillow gives a slice to the listing brokerage? Is it any listing Zillow “sold as leads” to Zillow Premier, Flex agents that did not close? Seller Brokerage Comp for advertising on Zillow.

Most important question did the home seller indicate to the listing agent / listing brokerage that their home would be syndicated to Zillow and many other sites? If yes, what is your payment / refund for the impact to the sale of your home when the Zillow feed was cut by the MLS? When did the utility technology supplier become the policy maker for the industry? Where is the MLS accountability?

I’m in the industry and it makes my head spin trying to keep track of what displays where, when are listing flows being cut from Zillow, etc. I get it, you just want your home marketed and sold professionally.

THE LAND GRAB — AND WHAT 100+ BROKERAGES JUST REVEALED

When the Chicago feed went dark, the response told you exactly who is building what — and why.

When MRED suspended Zillow’s access on May 20th, more than 100 brokerages picked up the phone and called Zillow — not the MLS, Zillow — to establish direct feeds and sign multi-year agreements so their listings would reappear AND when “the easy button to tour” is clicked on their listings, their agent is the one contacted, not the usual Zillow Subscribing Premier or Flex Agent.

The honorable reason is real. Fiduciary duty requires keeping a client’s home visible on the largest search site in the country, and no working agent could look a seller in the eye and explain why a corporate dispute had made their home invisible online.

But ask the harder question: why was Zillow actively messaging brokerages to sign? And why were so many brokerages so quick to protect the pipe?

The mechanic underneath has two layers. Layer one is fiduciary — the seller’s visibility must be restored. Layer two is the lead-revenue machine. A large share of agents rely on Zillow-generated buyer leads — Premier Agent, Flex — to fuel their business. No listings feeding Zillow means no buyer traffic on those listings, which means fewer leads, which means a slower commission pipeline, not to mention Zillow’s revenue. The listings had to go back. The home is the bait that stocks the pond the agent then pays to fish in.

But wait, Layer three has been born out of this — revenue flowing to the listing brokerage is now being negotiated to now receive payment on those listings being sold by a Premier Agent, Flex. Zillow and the Brokerage capitalizing through the monetization of your listing as a lead to agents and a bonus to the brokerage holding the listing — not to you the homeowner. Or as the recipient of “easy button to tour” to receive double listing brokerage comp or be the one making the referral and thus listing brokerage comp.

Where are your priorities in this monetization of the sale of your home? How are these brokerage / MLS gymnastics impacting the sale of your home? Are you tracking the market interaction with my listing or your kick-backs for the use of my listing as content?

And notice what just happened structurally. One clean pipe — MLS to Zillow to advertise your home on the market— shattered into 100+ private pipes overnight. Fragmentation, born live. Zillow did not resist. Zillow encouraged it, because every direct deal cuts the MLS out and locks the brokerage to Zillow on multi-year terms. For Zillow, the blackout was not only a crisis. It was an opportunity.

THE RECEIPTS — WHO EXECUTES THE STRATEGY LOCALLY

The practice nobody can stop fighting about happens in less than 6% of the market — and the brokerage selling it loudest is not the one winning at it.

In Fairfax County in April, the homes that closed within 0–1 days on market — the behavioral fingerprint of a deal worked privately before it ever went public — totaled 288 transactions out of 4,947 total April closings. That is 5.8% of completed transactions. More than nine out of every ten Fairfax County homes sold the normal, open, on-market way.

And of that smaller slice, the leader was not Compass. The leader was Monument Sotheby’s International Realty, a true luxury brokerage where off-market sales make legitimate sense for high-profile homes and private sellers. Non-Subscribing Offices were second and Samson Properties was third leaving Compass fourth.

![]()

Now run the bigger arithmetic. Compass closed 21 of Fairfax County’s 288 pre-market transactions in April. That is 7.3% of the 0–1 day cohort, and less than half of one percent (0.4%) of all April Fairfax County closings. The brokerage funding a federal lawsuit, restructuring four large regional MLSs, and dominating the national real estate conversation executes the strategy it is fighting for roughly four out of every thousand local transactions. A lot of national noise for a vanishingly small local footprint.

That gap — between the volume of the conversation and the volume of the execution — is the most useful data point in this entire analysis. It tells you the dispute is not about scaling a proven strategy. It is about controlling the rules and monetization under which the strategy could expand.

THE PRICE STORY — WHERE THE PREMIUM LIVES AND WHERE IT GETS RECAPTURED

The premium is real. It just is not the premium the marketing claims.

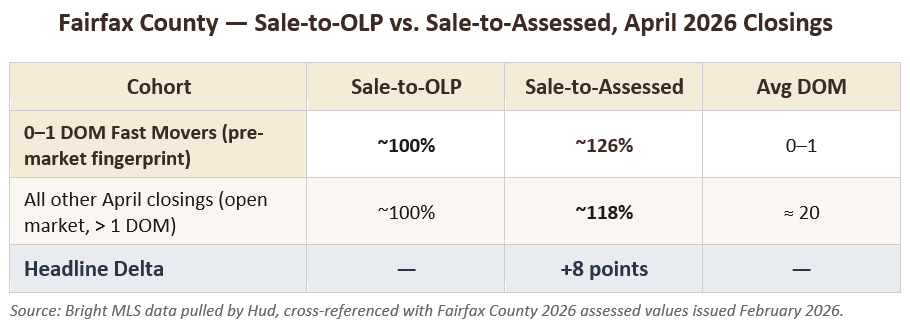

In Fairfax County for April, homes closed at roughly 100% of original list price and since it is entered and closed at once, they are one and the same in most cases — no pricing history. List price was an auction starting line, not a number to measure against. Sale price against the county’s assessed value told a different story.

The fast movers — the 0–1 day on market cohort — closed at approximately 126% of assessed value. Homes that closed on the open market after more than one day on market closed at approximately 118% of assessed value. A clean 8-point delta on the headline number.

The 8-point delta is real and should be reported honestly. It also is not the whole picture. The next layer of the data tells a different story — one that does not show up in the sale-to-assessed comparison because it lives in a separate line on the closing statement.

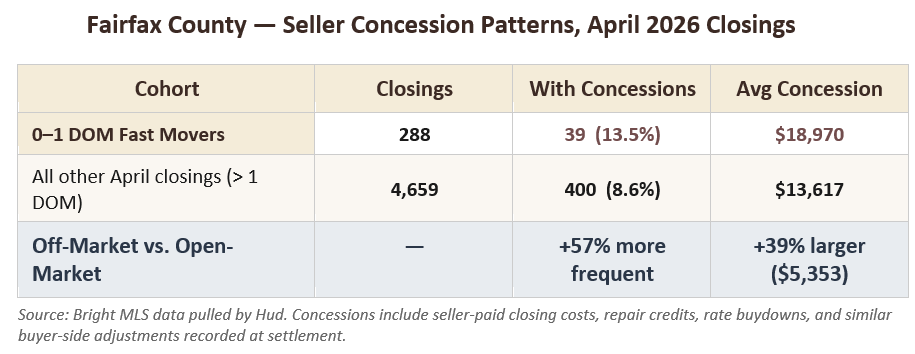

Pre-market deals also carry seller concessions to the buyer — closing-cost credits, repair credits, rate buydown contributions, and similar adjustments that reduce what the seller actually nets. The pattern is striking.

Two findings stand out: pre-market deals require concessions to close 57% more often than open-market deals, and when those concessions occur they average 39% larger — $18,970 vs. $13,617, a $5,353 average gap. The headline premium is partially negotiated back at the settlement table, in a line item less visible than the sale price.

The cleaner regional test exists, and Bright MLS already ran it. In April 2025, Bright analyzed more than 100,000 regional sales, controlling for location, condition, price point, and other variables.

The controlled finding: office exclusives sold 17 days slower than comparable open-market listings, with zero price advantage after the controls were applied. And 87% of office exclusives ended up on the open MLS anyway. That is the apples-to-apples comparison across a sample large enough to isolate the strategy’s actual contribution. The measured contribution is zero on price and negative on time.

So, what is the honest synthesis here. A genuine cream puff — a home in pristine condition, priced strategically, marketed with the full stack — can earn a premium in the current Northern Virginia market. I have won and sold it multiple times. That is a real outcome and the local data does not dispute it. We see it in pre-market deals and we see it on the open market. The premium itself is not the question.

The question is what produces it. When the cream puff sells through a pre-market channel, some of the premium reappears as concessions — more frequently, and in larger amounts. When the cream puff sells through open-market exposure, the same conditions hold and the regional control study finds no price advantage attributable to the strategy itself. The execution earns the premium. The concealment recaptures some of it on the way out.

What both numbers ARE measuring is a hot, inventory-starved spring market sitting on stale assessments. Both cohorts are paying multiple years of forward appreciation. The first ~10% above assessed represents the gap between the February 2026 assessment and true market value, since assessments lag the market. The next layer is pulled-forward appreciation at the prevailing 3% annual rate — roughly two to three years paid in advance for the open-market cohort, and additional years on top for the fast movers. A 118–126% premium this close to assessment date, in the full tilt of a spring market with inventory starved, is the market signaling at full power.

That signal is not created by concealment. It is revealed by exposure and full market positioning. The open market is the only place a premium of that magnitude becomes measurable for a typical seller, and the only place the concessions show up where everyone can see them.

A lot of national noise from one brokerage. Less than half a percent of the local market executing the strategy from the same brokerage. A modest premium on the headline number that gets partially negotiated back at closing. A regional control study finding zero price advantage attributable to the strategy itself. That is the entire price story.

THE NATIONAL PATTERN — A COORDINATED, REGIONAL CAMPAIGN

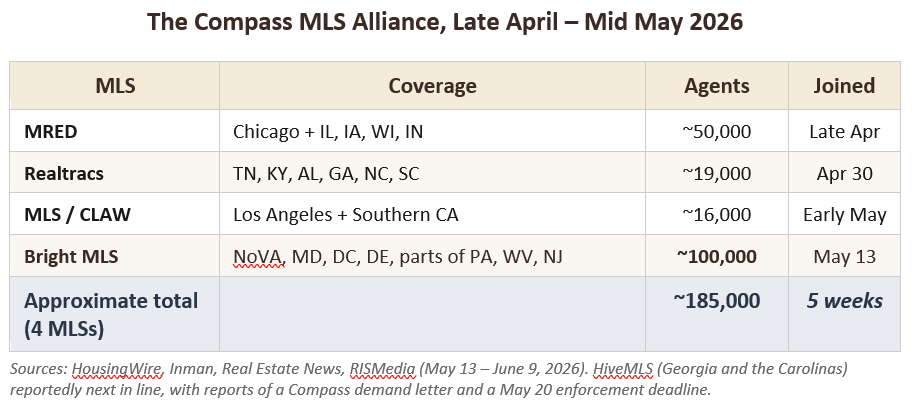

What started in Chicago is now visible as a coordinated rollout across four major U.S. regions.

In five weeks, Compass has secured partnerships with four of the largest regional MLSs in the country, each strategically positioned to cover a major U.S. market:

The geography is West Coast, Midwest, Central South, Mid-Atlantic.

On the May 5th Compass Q1 earnings call, Reffkin stated the strategy on the record: “We are bringing MRED national, as well as it will be just a select number of MLSs that are pro-seller choice, where we’re going to give them all of our listings, where we’re going to subsidize our agents joining. It’s not that I want to create a national MLS to replace local MLSs. I want to create a national MLS to compete against local MLSs.” Source: Motley Fool transcript, Compass Q1 2026 earnings call, May 5th, 2026. Compass is on the record naming itself as the orchestrator, naming the mechanic (subsidized memberships, all-Compass listings delivered to the partner MLS), and naming the goal.

The mechanic of each partnership is consistent. Compass subsidizes membership for its agents to join the partner MLS, then the partner MLS revises its IDX display rules in ways that conflict with Zillow’s listing standards. MRED cut its Zillow feed on May 20th. Zillow sued. A federal judge restored the feed on May 22nd. The lawsuit is active. Realtracs threatened the same cut for June 1st, extended the deadline to June 8th, and as of June 19th, still has not executed the cut while it negotiates a new licensing agreement with Zillow.

Realtracs has stated publicly that one primary goal of the new agreement is to ensure “brokers are compensated for their use of their listing content.” The negotiation is no longer only about display rules. It is also about a new commercial framework where the portal pays the MLS, which in turn compensates the brokers for the use of listing data. If Realtracs lands that arrangement, every other MLS in the partnership group has a template. DOJ ended the passing of funds from one brokerage to another with the NAR Antitrust Settlement in 2024. How does it become acceptable to pass funds from the Zillow Advertising Portal, to the MLS (the technology utility layer) and finally back to a listing brokerage where all three layers are working to define the rules that benefit themselves? Where is the oversight and financial checks and balances the NAR Antitrust Settlement put into place?

The leverage produced concessions without the feed being cut a second time. Threats issued without follow-through are still threats that move the negotiation.

Named industry voices are now publicly drawing the same line. Anthony Lamacchia, CEO of Lamacchia Realty operating across seven states, told RISMedia on June 9th: “On the MRED story, I do know — Compass was pulling the strings. I’m sure of that.” And on the broader question of who is hurt: “If a seller doesn’t have access to everybody, and a buyer doesn’t have access to all the properties, it’s hurting the client. If you’re a seller and you can’t get your property maximum exposure because a Zillow feed got shut off over a pissing contest between Compass and Zillow — that’s ridiculous.”

And on whether a “national MLS” even exists in any meaningful technical sense, Cameron Paine, CEO of the St. Louis-based MARIS MLS, told RISMedia: “I just want to push back on the whole name of the national MLS. There is no such thing. To be a national MLS, you have to have all the data, and no MLS has all the data. It feels more like a marketing play to me than reality.” That is an MLS CEO calling the framing what it is: a marketing play.

A regional MLS opening membership to agents nationwide is not the same thing as a national MLS — a fact the industry has begun naming out loud.

And here in Northern Virginia, Bright MLS finalized its Compass partnership on May 13th. Bright’s leadership has so far framed the partnership as cooperation. Bright extended its Coming Soon status to unlimited duration in May — a flexibility move for sellers, though Coming Soon still does not permit tours. That posture is genuinely different from MRED’s or Realtracs’. Whether posture continues to match play over the next quarter is the open question every Northern Virginia seller should be tracking.

What is no longer in dispute is the pattern: a coordinated, regional campaign to reshape both the rules and the economics of how listing data flows to the consumer search portal. Zillow’s federal lawsuit against Compass and MRED characterizes it as “coordinated market power.” A federal court will eventually decide whether that legal frame applies. The behavioral pattern is no longer hidden.

WHAT WINS — THE 4 P’S OF MARKETING

The premium is real. It is earned by execution in the open market, not by concealment.

A well-executed pre-market strategy can work. I have represented buyers and won that had great pre-market strategies. The win is not about hiding — it is about four levers, executed together:

▸ Condition (Product). A home that is pristine, maintained, renovated and move-in ready removes every reason a buyer hesitates. This is the lever average agents skip. The cream puff effect lives here. Price always reflects the condition the home is in.

▸ The full marketing stack (Positioning): professional photography, video, 3D tour, floor plan, lifestyle targeting. Most “Coming Soon” listings in any given market arrive without these – that’s announcing not positioning and inviting the targeted buyer in. Across recent Fairfax County Coming Soon listings, the count of full 3D-plus-video-plus-floor-plan packages was small enough to count on one hand. In a fast moving market, average agents will save on the expense – it will sell fast, but did it sell for the most competitive price is the question? The brokerages claiming a pre-market advantage frequently do not bring pre-market-grade marketing.

▸ A pricing strategy (Pricing) that lets the market push the value up, not an out-of-the-gate overprice that sits and then reduces to the same number a well-priced home would have hit in a week.

▸ Pre-marketing (Promotion) done in the open, with intent, fully visible to every cooperating agent — not as concealment dressed up as strategy. Coming Soon is the invitation and going Active is the start of the Main Event.

A home sells for similar money in five days or fifteen days. The difference is execution. The home that sits and reduces ends up at roughly the same number the sharp one earned, minus the holding cost and the stress. Concealment does not create the premium. Execution does.

THE SYNTHESIS — WHO PAID, WHO IS PAYING NEXT, AND THE OPEN QUESTIONS

Walking the receipts forward into the read.

▸ The seller paid first. 43,000 Chicagoland sellers (and an equal, if not double the number of home buyers) were made temporarily invisible on the largest consumer search platform in the country on May 20th over a dispute their listing agreements did not contemplate, much less disclose — and tens of thousands more across six Southern states have been kept under that threat through two consecutive deadlines in a game of Chicken to see who blinks first.

▸ The portal is paying with leverage. Zillow’s federal lawsuit alleges “coordinated market power.” A judge has already granted one temporary restraining order. The licensing economics are now in negotiation. The portal’s data-pipe dominance is being tested for the first time in 15 years. The deeper contradiction sits in the timeline: Compass sued Zillow last year for restricting pre-market listings, won the policy change, dropped the case — and is now orchestrating MLS partnerships to cut the same portal it fought to be on. On the portal or off — pick one.

▸ The brokerage is paying for the strategy out of marketing dollars, legal fees, and subsidized MLS memberships, while executing the strategy on less than half of one percent of completed local Fairfax County transactions and watching a regional control study show no price advantage attributable to the strategy itself.

▸ The MLS is paying with mission risk. Every cooperative-model MLS is now answering for whether it is a neutral infrastructure utility or a coordinated commercial actor.

Let a Coming Soon listing be marketable, visible, AND tourable across every subscribing brokerage.

Done. Sellers keep their privacy options. Buyers see every available home. No brokerage gets to build a hidden funnel. The MLS stays exactly what it’s supposed to be — a neutral utility serving every agent equally, not a policy maker.

THE BOTTOM LINE

What this means for you, practical implications.

For Northern Virginia homeowners considering a sale: ask your agent the questions this story has surfaced:

- What is your plan to make my home visible if any portal feed gets disrupted?

- How does your brokerage make money from my listing besides the commission on its sale?

- What pre-market marketing do you deliver?

- What are the outcome based measurements behind the strategy versus open-market sales? Speed, concessions, appraisals and appreciation.

- Are you tracking the market interactions with my listing or are you focused on tracking the kick-back my listing as content generates?

Working agents who operate in primary-source data will have direct answers.

For buyers: the easy-button “schedule a tour” click does not connect you with the home’s listing agent or with an agent who represents your interests. Ask who you are speaking with, who pays them, and what their fiduciary obligation to you is — before you share contact information or visit a property.

Whew, that was a lot are you still following? As my father always said, “Nobody got anywhere fast on a short-cut”.

Netting this out, there is an enormous amount of time, money and consumer impact being spent to game a market for personal interests. The key is uncovering the motivations of the agent / brokerage you choose to do business with – are they hard working agents focused on the consumer or are they creating complicated policies and strategies to line their pockets at the consumer’s expense.

Series — Where This Sits:

Part 1: Buyers Locked Out: Two Billionaires Are Fighting Over Your Listing — published on RealEstateofNVA.com.

Part 2: This post.

Part 3 (planned): If We Rebuilt the System Today: A Clean-Sheet Read on Consumer Real Estate Search. The constructive companion to Parts 1 and 2.

Michele Hudnall

I Guide. You Decide. Equity Focused Always.

Real Estate of Northern Virginia | Equity-First Real Estate Strategy

[email protected] | 703.867.3436

RealEstateofNVA.com | @realestateofnva

I help Northern Virginia buyers and sellers make smarter decisions with local market analysis, strategic guidance, and real-world context supported by current market behavior, not hype headlines.

If you want a clear read on your home, your neighborhood, or your next move, let’s talk.

Disclosure: Michele Hudnall is a licensed real estate agent in Virginia. This post represents her personal analysis and good-faith opinion as a Reston resident and does not constitute legal or financial advice. Full disclosure at RealEstateofNVA.com. All analysis and opinion are my own and based upon local, real-time data. Please consult with a financial or legal professional as required.

Privacy Statement | Disclosure Notice

METHODOLOGY

This post combines national reporting from named, freely-accessible sources with original Fairfax County and Reston market research drawn from Bright MLS data covering April 1 – May 6, 2026.

Local data was pulled directly from Bright MLS reports for the April 1st – May 6th, 2026 window. The Fairfax County 0–1 days-on-market subset (288 transactions) was extracted from the full April closed pool of 4,947, and aggregated by listing brokerage. The sale-to-assessed comparisons were calculated against Fairfax County’s 2026 assessed values (issued February 2026). Seller concession data was pulled at the transaction level and aggregated by frequency and average amount for each cohort. Pre-market share of 5.8% is calculated on completed closings, not on broader activity.

The Hud Market Value Anchor (assessed × 1.10 ≈ market value) is grounded in Fairfax County assessor methodology, which targets assessments within 10% of market value. The framework treats the first ~10% over assessed as the gap-to-market correction, the next ~10% as pulled-forward appreciation at the prevailing 3% normal annual rate, and additional points as further forward-pulled appreciation.

Cross-validation: the 2026 local findings independently replicate Bright MLS’s April 2025 statistical study of more than 100,000 sales (“Impacts of Office Exclusives”). Two data sets, one year apart, directionally identical conclusion.

SOURCES

▸ The Motley Fool — https://www.fool.com/earnings/call-transcripts/2026/05/06/compass-comp-q1-2026-earnings-call-transcript/ — Compass (COMP) Q1 2026 Earnings Call Transcript, May 5, 2026 — primary-source transcript containing the Reffkin national-MLS statements verbatim.

▸ CNN Business — https://www.cnn.com/2026/05/20/business/zillow-compass-private-home-listings-lawsuit — “Thousands of Chicago-area home listings just went dark on Zillow,” Samantha Delouya, May 20, 2026 — primary reporting on the MRED feed cut, the 5,000-to-2,000 Chicago listing drop, and the 3-of-17 MRED board seat allegation.

▸ The Real Deal — https://therealdeal.com/chicago/2026/05/22/judge-orders-chicago-mls-to-restore-zillow-access-to-listings/ — “Judge orders Chicago MLS to restore Zillow access to listings,” May 22, 2026 — the federal TRO, the 43,000-listing figure, and the detail that the disputed listings were in Florida, Georgia, and California.

▸ Real Estate News — https://www.realestatenews.com/2026/06/01/zillow-will-retain-access-to-realtracs-listings-for-now — “Zillow will retain access to Realtracs listings — for now,” Lillian Dickerson, June 1, 2026 — the Realtracs deadline extensions and the broker-compensation principle in the new licensing negotiation.

▸ RISMedia — https://www.rismedia.com/2026/06/09/the-national-mls-doesnt-exist-yet-but-the-fight-over-it-is-already-here/ — “The National MLS Doesn’t Exist Yet. But the Fight Over It Is Already Here,” Clarissa Garza, June 9, 2026 — named-broker reporting from Lamacchia, Hanna, Paine, McCann, and Troup.

▸ Inman — https://www.inman.com/2026/05/06/reffkin-sheds-light-on-compass-push-for-national-mls-we-are-bringing-mred-national/ — Reffkin sheds light on Compass push for national MLS, May 6, 2026 — contemporaneous coverage of the Reffkin earnings-call statement.

▸ HousingWire — https://www.housingwire.com/articles/cms-2026-mls-alliance/ — MLS-led alliance analysis — the full four-MLS alliance summary and the seven-day timeline from earnings-call statement to federal antitrust filing.

▸ Real Estate News — https://www.realestatenews.com/2026/05/13/beyond-the-noise-what-brokers-should-expect-from-an-mls — Brian Donnellan op-ed, May 13, 2026 — Bright MLS CEO’s announcement of the Compass partnership and the cooperative framing.

▸ FTC.gov — https://www.ftc.gov/news-events/news/press-releases/2025/09/ftc-sues-zillow-redfin-over-illegal-agreement-suppress-rental-advertising-competition — “FTC Sues Zillow, Redfin Over Illegal Agreement to Suppress Rental Advertising Competition,” September 2025 — primary-source documentation of federal antitrust action concerning portal competition.

▸ CNN Business — https://www.cnn.com/2026/04/26/business/robert-reffkin-risk-takers — “Robert Reffkin is changing the way Americans buy homes,” Samantha Delouya, April 26, 2026 — the “agent is the client” quotation and the “killer of value” characterization.

▸ Bright MLS / Lisa Sturtevant, PhD — “Impacts of Office Exclusives,” April 2025 — Bright MLS statistical study of 100,000+ sales finding office exclusives sell 17 days slower with zero price advantage, and 87% surface on the open MLS within the transaction cycle.

▸ Original research — Fairfax County and Reston Bright MLS data, April 1 – May 6, 2026, pulled directly by Hud. Aggregated brokerage rank of 0–1 DOM transactions, sale-to-assessed comparisons, seller concession analysis, and Coming Soon marketing-tool inventory are all primary.